Kapitalbeteiligung effizient nutzen

Global Shares wird zu J.P. Morgan Workplace Solutions. Verbessern Sie Ihr Kapitalbeteiligungsangebot mithilfe von Lösungen, die auf die Bestärkung Ihrer Mitarbeitenden ausgelegt ist und Ihre Vergütungsstrategie zum Leben erweckt.

Unternehmen weltweit

vertrauen uns

Mehr als nur ein Anbieter

für Kapitalbeteiligung

Unsere Plattform unterstützt Ihr Team dabei, den aktuellen und potenziellen Wert ihrer Vergütungen zu verstehen. Mit einer intuitiven Technologie, die Beteiligten einfachen Zugriff auf ihren Kapitalbesitz, finanzielle Weiterbildung und Einblicke bietet. Unsere Teams werden zu einer Erweiterung Ihrer Teams und unterstützen Beteiligte in wichtigen Momenten mit einer umfangreichen Verwaltung und einer Plattform, die sich in Ihre HRIS- und Steuersysteme integrieren lässt

Vereinfachte Verwaltung und Berichterstellung für Kapitalbeteiligung

Gewährt Mitarbeitenden Transparenz und Einblicke in ihre Vergütung, fördert ein gesteigertes Engagement und Bindung ans Unternehmen

Bietet eine intuitive Erfahrung für Beteiligte zur vereinfachten Verwaltung von Zuschüssen und Übertragungen sowie Weiterbildungen und Support

Bietet professionelle Services für Ihre Geschäftsführung und Leitung

Bietet interaktiven Support für Sie und Ihre Mitarbeitenden

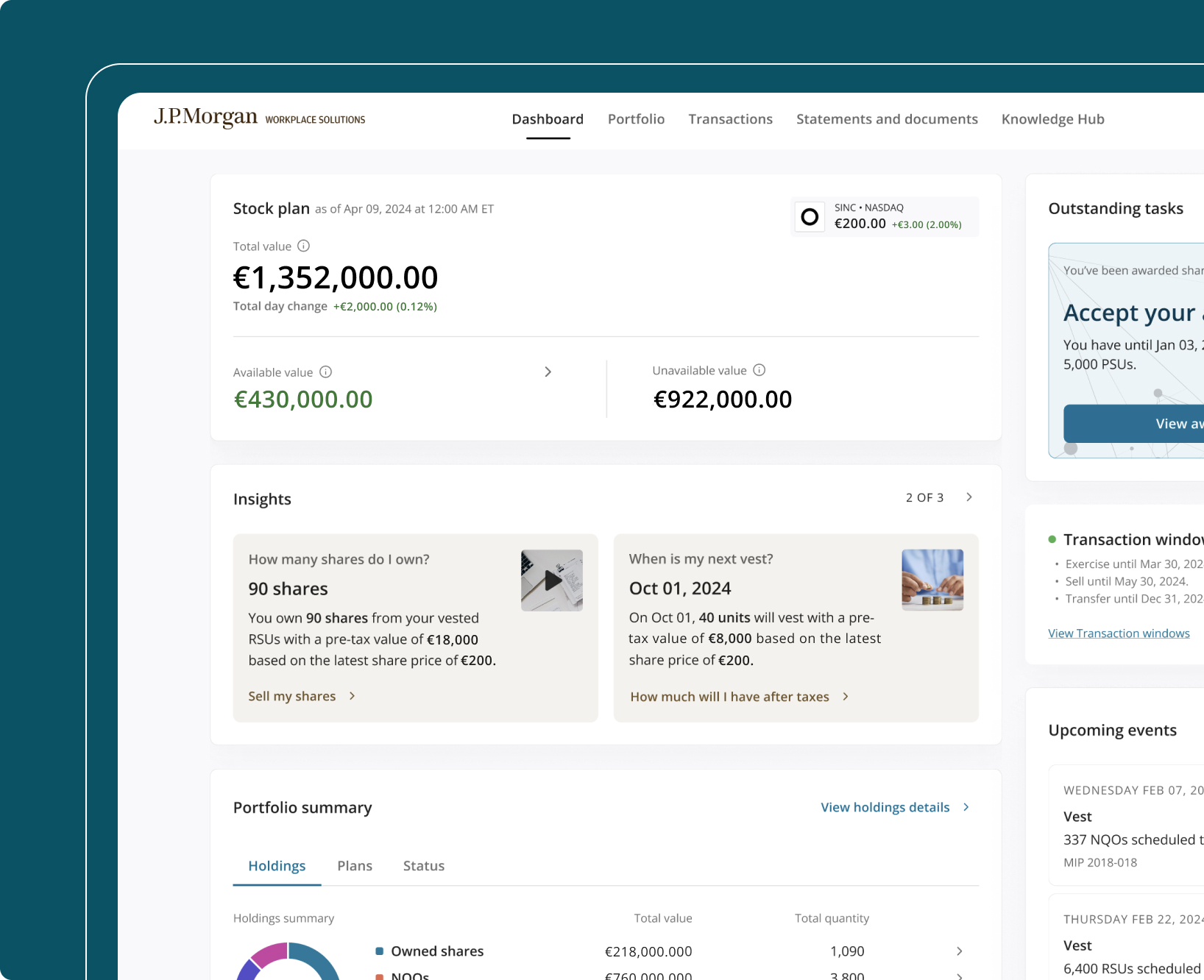

Kapitalbeteiligung

Komplette Service-Administration Ihrer globalen Beteiligungsprogramme für Ihre Mitarbeitenden sowie einfachen Zugriff für Beteiligte auf die Transaktion ihrer Vergütungen. Engagierter Support für Sie und Ihre Mitarbeitenden.

Unterstützt von Global Shares

![]()

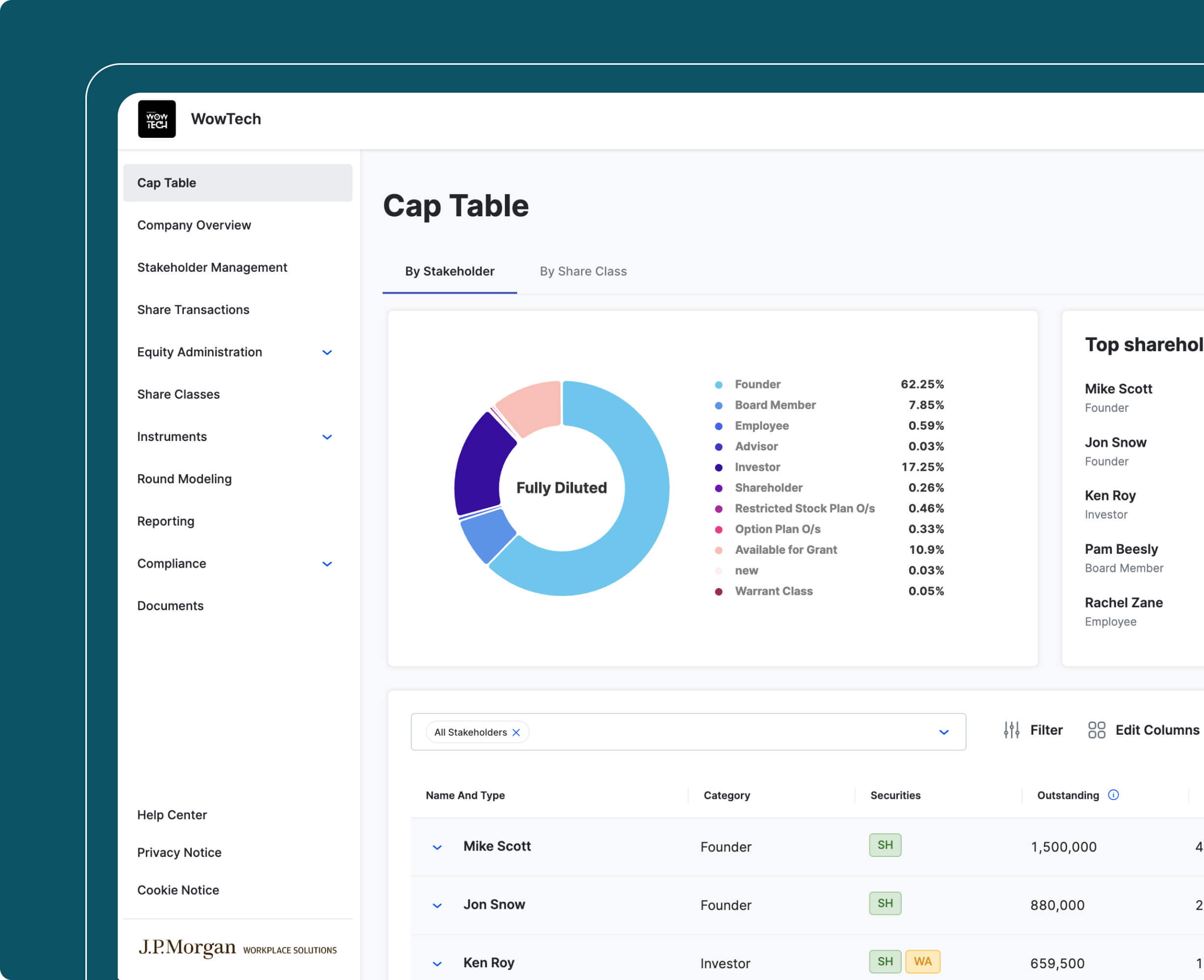

Verwaltung

von Cap table

Sorgen Sie für eine solide Wachstumsgrundlage, um Ihr Unternehmen durch Finanzierungsrunden, künftige Liquiditätsereignisse und mehr zu begleiten. Unsere digitale Plattform dient als Single-Source-of-Truth für Investoren und Mitarbeitende und ermöglicht die vereinfachte Verwaltung des Mitarbeiterkapitals.

Unterstützt von Global Shares

![]()

Wir gestalten die Kapitalbeteiligung ganz einfach

Unsere Plattform zur Verwaltung der Kapitalbeteiligung für private und börsennotierte Unternehmen ist so gestaltet, dass sie alle Kategorien Ihrer Kapitalbeteiligungspläne weltweit verwaltet. Bestärken Sie Ihre Teams durch zweckbestimmten Support, der darauf spezialisiert ist, Ihre Mitarbeiter zu inspirieren und Ihre Vergütungsstrategie in die Tat umzusetzen.

Vorteile

-

Talente

Interessieren, inspirieren und halten Sie talentierte Mitarbeitende, die genauso an Ihr Unternehmen glauben, wie Sie an sie.

-

Integrität

Eine Single-Source-of-Truth für all Ihre globalen Mitarbeiterdaten. Vereinfachte Ausgabenarchivierung, Offenlegungen, Steuerabgrenzung und EPS-Berichte.

-

Professionelle

UnterstützungAccount Manager und Kapitalexperten zur Unterstützung aller Plankategorien.

-

Berichterstellung

Intuitive Business Intelligence Berichterstellung bietet Ihnen authentische Einblicke in Ihr Unternehmen. Mehr Transparenz in Bezug auf Erdienungszeiträume, Ablaufvorschriften, Gewährungen, Vergütungen und Veranstaltungen.

Unterstützung für

Ihren Erfolg

Unabhängig von Ihrer Rolle.

-

HR-Fachkräfte

Sie bekommen einen eigenen Account Manager an die Seite gestellt und erhalten Zugriff auf ein Team aus professionellen Kapitalexperten, die Sie bei der täglichen Bewältigung Ihrer Pläne unterstützen. Ihre Mitarbeitenden erhalten zudem Support von unserem mehrsprachigen Kundenservice.

-

Rechtsabteilungen

Die Gewissheit, mit einem vertrauenswürdigen Anbieter zusammenzuarbeiten, der die Compliance Ihrer Beteiligungspläne gewährleistet, ganz gleich wo Ihre Firma tätig ist, ermöglicht einen wunderbar sorgenfreien Arbeitsalltag.

-

Finanzabteilungen

Unsere Technologien automatisieren und optimieren die Verwaltung von Beteiligungsplänen und ermöglichen API-Integrationen mit Ihren HRIS- und Steuersystemen. Unsere integrierten Funktionen zur Berichterstellung ermöglichen Ihnen das Generieren Audit-fähiger Berichte mit nur wenigen Klicks.

-

C-Suite

Sie wollen sicher vermeiden, dass den Ambitionen Ihres Unternehmens Steine in den Weg gelegt werden. Wir können Ihnen helfen, sich vom privaten zum börsennotierten Unternehmen, von einer lokal zu einer global tätigen Firma zu entwickeln: Mit einer grenzenlosen Kapitalbeteiligungsverwaltung.

Bereit, Ihre

Kapitalbeteiligungsstrategie

zu transformieren?

Erfahren Sie, wie wir Ihre Kapitalbeteiligungsverwaltung

vereinfachen können